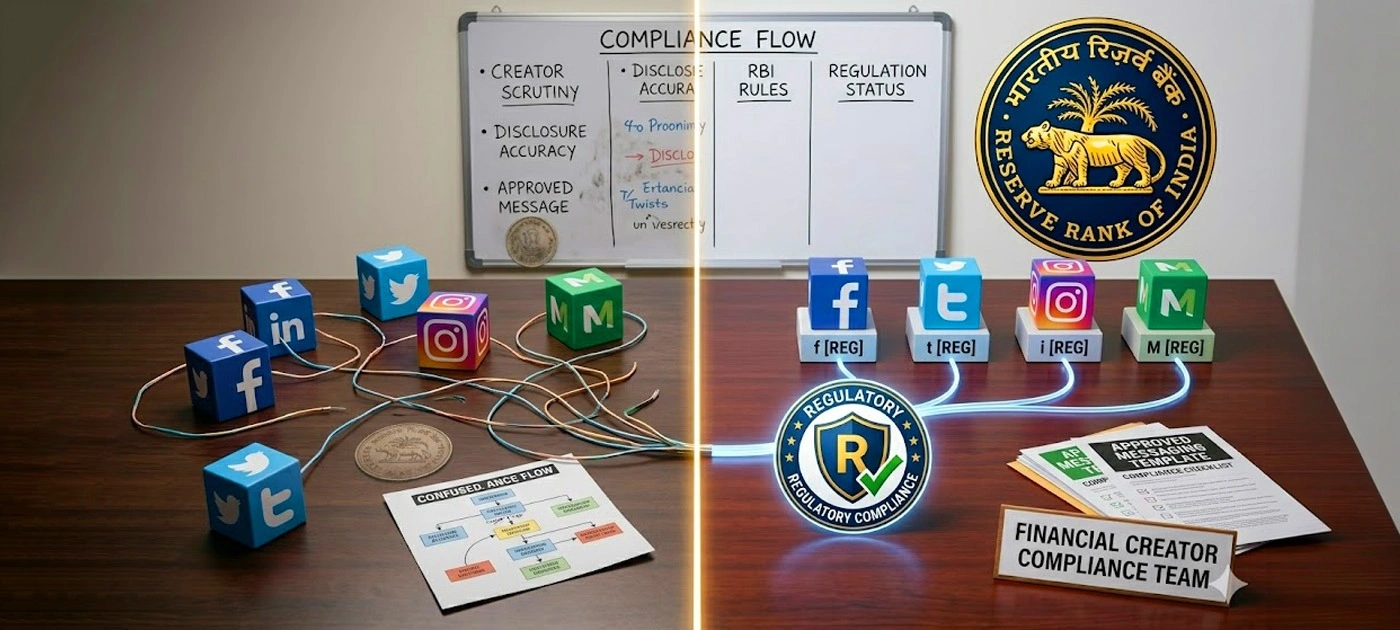

RBI has introduced a regulatory framework to crack down the misselling of financial institutions. This new directive specifically addresses the marketing of investment tools, insurance, credit services, and payment cards by various entities and individuals.

Starting January 1, 2027, if a bank or NBFC hires an agent to promote the product, whether a finance creator, a lifestyle influencer, or an affiliate marketer, that bank is legally responsible for everything they say. Under the view of the regulatory authority, these influencers essentially function as the formal representatives of those institutions.

What changed

The RBI’s new directions apply to banks, NBFCs and major wholesale lenders including NABARD, NaBFID, NHB and EXIM Bank. Regardless of the sales channel be it a physical branch, a mobile application, or a digital platform like YouTube/Instagram, the framework maintains its neutral stance.

The regulator has also explained the definition of misselling to include pushing products that do not match a customer’s income or risk profile, sharing incomplete information, selling without recorded consent, and forcing customers to buy bundled products they never asked for.

What this means for creators

Post RBI notification June 2026, financial institutions are now going to be far more careful about who they partner with. Creators in the industry can expect tighter briefs, stricter compliance reviews, and brands scrutinising every claim made in sponsored content. Deals where messaging cannot be controlled will likely be dropped altogether.

Financial and fintech creators should proactively upgrade their professional standards before new compliance mandates take effect. It is essential to ensure precise product claims, maintain records of approved scripts, and provide clear, prominent disclosures.

What happens in case of misselling

If misselling is established, the customer will be entitled to a refund of the entire amount paid for the product. The lender will also have to inform the customer about cancellation of the sale and compensate for losses arising from the transaction, according to the RBI framework.

Previously, customers often faced difficulties in proving they were misled after agreeing to complex terms. Consequently, customers can review all product documentation, including charges, risks, and exit conditions, before digital approval, while cautioning against coerced product bundling and advising the maintenance of records for all sales-related communications.

Furthermore, although the RBI framework does not impose direct penalties on creators, it elevates their role in regulatory risk management, making those who prioritize accuracy and transparency increasingly valuable in this evolving compliance landscape.